While economists predict inflation in Canada will stabilize, the rate will continue to remain higher than an ideal target.

Organizations of all sizes will not only have to navigate how this impacts their operations as a whole, but also shift how they support their employees’ needs in an ever-changing health and wellness environment.

As such, Acera Benefits — a leader in the Canadian group benefits market — advises employers to examine their group plans in 2024 with a critical eye on the following areas:

Escalating Costs

The cost of administering a competitive employee benefits plan is increasing as inflation drives costs for prescription drugs and other services (i.e., dental care, paramedical practitioners) and plan members submit more claims for their shifting health and wellness needs (i.e., mental health, chronic health conditions). For example:

Dental fee guide increases in 2023 ranged between 5% and nearly 10% across Canada, compared to 1% and 5% annually between 2017 and 2021. Furthermore, insurers anticipate the frequency of dental claims will increase between 4% and 7% in the coming year, which is in addition to the pressure from fee guide increases.

Over 50% of Canadian group plan members live with at least one chronic health condition; of those with a chronic condition, nearly 80% take at least one medication on a regular basis.

An increase in adults being diagnosed with diabetes, ADHD and asthma saw claim costs for these treatments increase by 17%, 22% and 17%, respectively, in 2022.

The average amount covered for paramedical services in 2022 was $458 for each plan member — nearly a 10% increase compared to 2021, driven primarily by inflation.

These factors are challenging the long-term sustainability for many employers’ group benefits offerings, but there are ways to balance escalating costs with employees’ greatest needs.

Diabetes: The Rise of Ozempic

With one in three Canadians having either prediabetes or diabetes, most insurers have committed to covering Ozempic when it is used to treat the disease.

This is in response to the average covered claim amount for the prescription drug skyrocketing by 85% in 2022, thanks in large part to aggressive advertising campaigns and attention-grabbing headlines about Ozempic contributing to weight loss.

Acera Benefits advisors can help your organization design and administer a cost-effective group plan by utilizing different formulary options, leveraging government and patient assistance programs, and adjusting your plan based on claims usage.

Supporting Employees’ Financial Wellness

Inflation is forcing Canadians to spend more on essential expenses like housing and groceries, and significantly reducing their ability to save for the future.

This means, now more than ever, employers need to consider group retirement savings plans as a key component of their recruitment and retention strategy — employees and candidates are expecting it.

In fact, 74% of Canadian workers say it’s important for employers to offer a savings option.

To keep pace with the competition, employers who have not previously offered a group retirement savings plan will need to implement one. Other organizations will want to consider increasing contributions to their existing group retirement savings plans to further stand apart from the competition.

Acera Benefits advisors can offer several creative strategies to help your organization mitigate the financial impact of implementing or expanding your group retirement savings plan.

Budgeting for Second CPP Contributions

As of Jan. 1, 2024, both employees and employers will have to make an additional 4% contribution to the Canadian Pension Plan for those who earn between the first earning ceiling and the new second earning ceiling. The example calculation illustrates the 2024 tax implications of this new requirement.

While the second CPP contribution is relatively small, it may impact an organization’s budget for its overall benefits and group savings programs.

Example Calculation for 2024

Second earning ceiling $73,830

First earning ceiling – $69,000

Taxable difference $4,830

Taxable difference $4,830

Second CPP contribution rate x 4%

Second CPP contribution per eligible employee

$193.20

Acera Benefits advisors can help your organization design and administer a cost-effective group plan by utilizing different formulary options, leveraging government and patient assistance programs, and adjusting your plan based on claims usage.

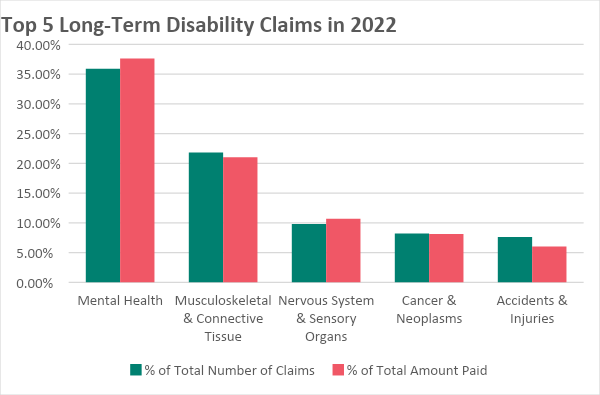

Growing Mental Health Challenges

Personal finances are a significant cause of stress, so it’s no wonder that rising costs and dwindling savings are affecting the mental health of an ever-growing number of Canadians.

An increase in mental health conditions — including depression, anxiety and adjustment reaction — have resulted in the steady growth of group plan claims being submitted and paid, year-over-year. This has resulted in mental health conditions being the most common long-term disability claims expense.

Mental health also takes a toll in the workplace:

- Half of millennial and three-quarters of Gen Z employees have left their job due to mental health challenges.

- Depression can interfere with a worker’s ability to do their job, reducing cognitive performance more than one-third of the time.

- Half a million Canadians miss work every week due to mental illness.

This trend cannot be ignored and deserves to be thoughtfully considered by employers when it comes to designing, revising or expanding a group benefits plan.

Acera Benefits advisors can help you find solutions that go beyond offering traditional employee and family assistance programs to ensure your workers have access to the mental health support they need most.

Employee Wellness & Wellbeing

Employees — younger ones in particular — continue to place less value on traditional group plans and are increasingly expecting their employers to proactively contribute to their overall health and wellbeing.

In response, your organization may want to expand coverage for popular paramedical services and/or implement spending accounts that employees can use towards their self-improvement.

Cost Effective Solutions for Your Organization

Acera Benefits will support you in designing and administering a meaningful and competitive benefits plan that addresses the unique requirements of your organization and employees.

We bring decades of experience in providing trusted advice and guidance to Canadian organizations of all sizes, creating customized solutions to help employers maximize the return on their investment for healthier, happier and more productive employees.

Let’s discuss what we can do for you.

Disclaimer: This document is advisory in nature. It is offered as a resource to be used together with your professional insurance and legal advisors in developing a group benefits program. This guide is necessarily general in content and intended to serve as an overview of the risks and legal exposures discussed herein. It should not be relied upon as legal advice or a definitive statement of law in any jurisdiction. For such advice, an applicant, insured or other reader should consult their own legal counsel. No liability is assumed by reason of the information this document contains.