After years of hard insurance market conditions and record-breaking natural catastrophes, 2025 offered Canadian businesses some reprieve.

Now, as we look to 2026, the overarching guidance from Acera Insurance advisors is to avoid complacency. Their insights emphasize how staying diligent about loss prevention and taking advantage of favourable rates can strengthen your business outlook for this year.

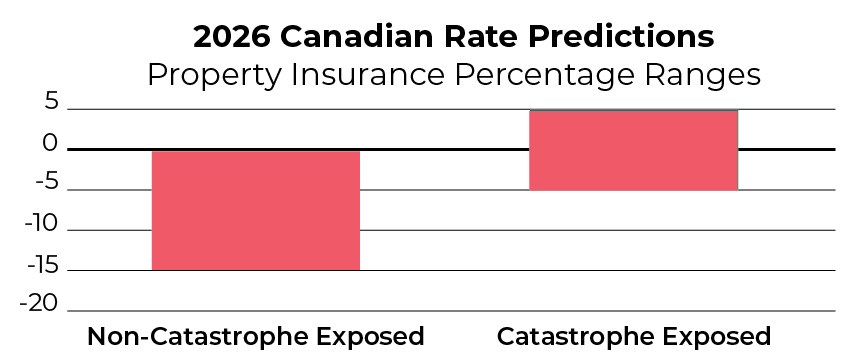

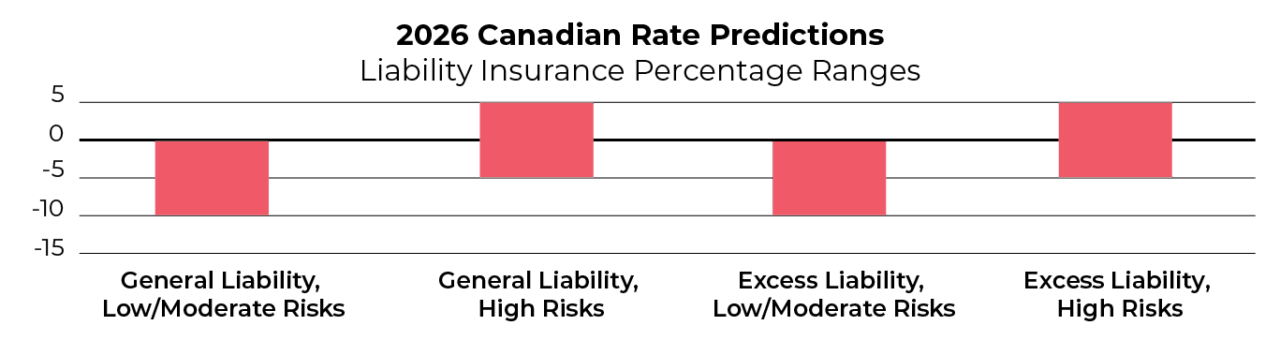

Soft market

Insurers predict that soft market conditions in Canada will continue in 2026, providing competitive rates and the greater ability to secure coverage.

Note: Estimated rate increases/decreases are averages across all industry segments, and rate increases/decreases can vary widely based on the industry class, risk quality and loss history.

Increased market capacity, less stringent underwriting standards and aggressive pricing provides several benefits, with many businesses zeroing in on the potential cost savings.

But there’s danger in assuming lower premiums mean lower risks.

Choosing a quote based on price alone can come at the cost of coverage scope, possibly leaving you more exposed than in the past. Instead of only looking at competitive pricing as a cost savings opportunity, approach the soft market as an optimal time to invest in broader protection — such as higher limits, new coverage lines and multi-year policy deals.

More relaxed underwriting can also undermine the importance of risk management; however, the longevity of your business relies on its ability to both mitigate and rebound from losses. Ongoing investments in loss prevention and updating emergency response plans must remain a priority.

As your business approaches its 2026 renewal, look at the soft market holistically to strike the right balance between premium savings and enhanced protection.

“Which insurer offers the most appropriate coverage? Who has a better track record for paying claims? Is one policy wording stronger or broader than another? These differences can be far more important in the event of a claim than a 5% premium saving.”

Janelle Lordon Director, Complex Risks

How to protect your business

Carefully review your policy wording to ensure it meets your coverage requirements, not just your budget.

Consider increasing coverage limits, updating valuations and adding new lines while premiums are favourable.

Prioritize insurer financial strength and long-term stability over short-term savings.

Maintain strong risk management practices and communicate them to underwriters to secure favourable terms.

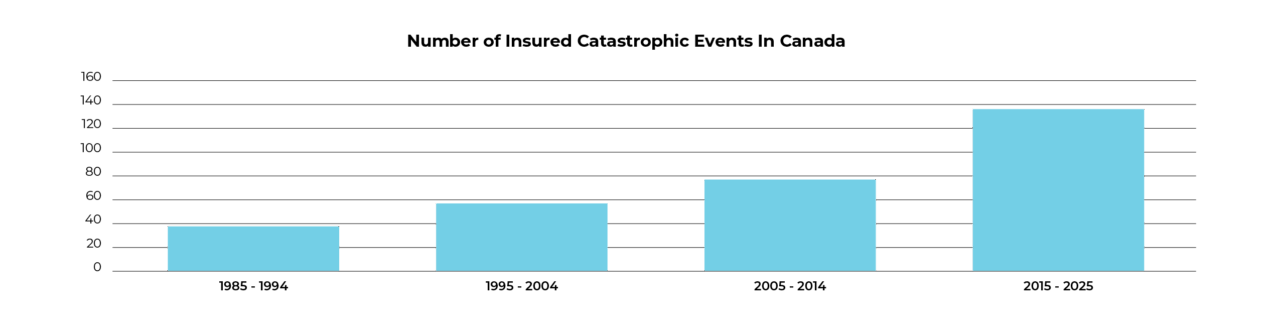

Natural catastrophes

One area where strict underwriting remains is natural catastrophe exposures.

While insured losses caused by severe weather in 2025 paled in comparison to Canada’s $9.2 billion record-breaking year in 2024, three noteworthy events were significant:

Ice storm in Ontario and Quebec, resulting in approximately $342 million in insured losses.

Wildfires across Manitoba and Saskatchewan, resulting in nearly $300 million in insured losses.

Wildfire in Newfoundland and Labrador, resulting in more than $70 million in insured losses.

Where wildfires are concerned, 2025 is Canada’s second-worst wildfire season on record, in terms of hectares burnt. More stark is the fact that wildfires blazed across regions once considered lower risk: Saskatchewan, Manitoba and the Atlantic provinces.

Severe weather has become the norm. This, along with the looming risk of a large earthquake striking the West Coast, continues to make underwriters cautious when it comes to insuring property in risky areas.

Preparing for the year-after-year barrage of natural catastrophes is starting to take a toll and we’re seeing fatigue set in around disaster preparedness.

But neglecting pre-loss planning, delaying infrastructure upgrades or overlooking emergency response protocols increase the risks of slower recovery, higher claim costs and significant disruption when the next event strikes.

Insurers also continue to impose strict deductibles, exclusions and geographic limitations for properties located in high-risk areas. So, remaining diligent about proactive disaster preparedness and demonstrating strong loss prevention measures is critical for securing more favourable terms and adequate coverage in such locations.

“Insurers are tightening underwriting for catastrophe-prone areas, making preparedness a key differentiator for coverage and pricing.”

Leah Wood Director, Claims & Loss Control

How to protect your business

Enhance catastrophic planning, using updated tools and walkthroughs.

Leverage vendor service level agreements and rapid response programs to minimize the impact a natural catastrophe could have on your business.

Continue to invest in mitigation measures, such as installing flood, fire and hail protection systems.

Document and communicate your risk mitigation measures with underwriters to secure better insurance terms and coverage options.

Cybercrime

While ransomware attacks and social engineering still dominate, cybercriminals are constantly adapting to exploit organizations’ reliance on technology — and the following three emerging risks are likely to continue to evolve in 2026.

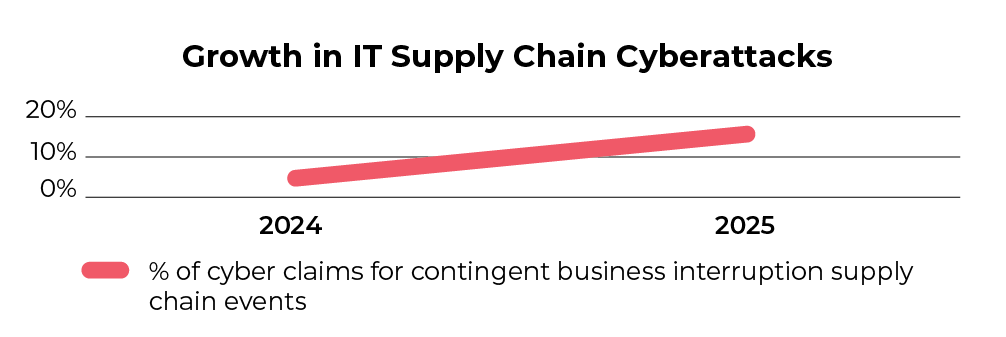

1. IT supply chain attacks

It’s not just your own systems and networks that you have to worry about. Cybercriminals are increasingly targeting supply chains to maximize their windfall from every breach. The ripple effect of cyberattacks on third-party vendors can be felt far and wide and quickly lead to operational downtime and lost revenue for your organization.

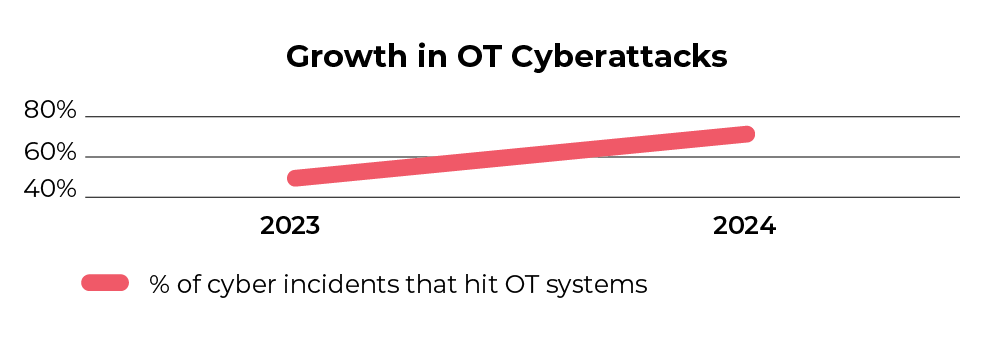

Cybercriminals are no longer solely focused on stealing data; they are increasingly targeting operational technology. With this comes a rapid rise in attacks that have physical consequences, including equipment damage, service disruption and safety hazards.

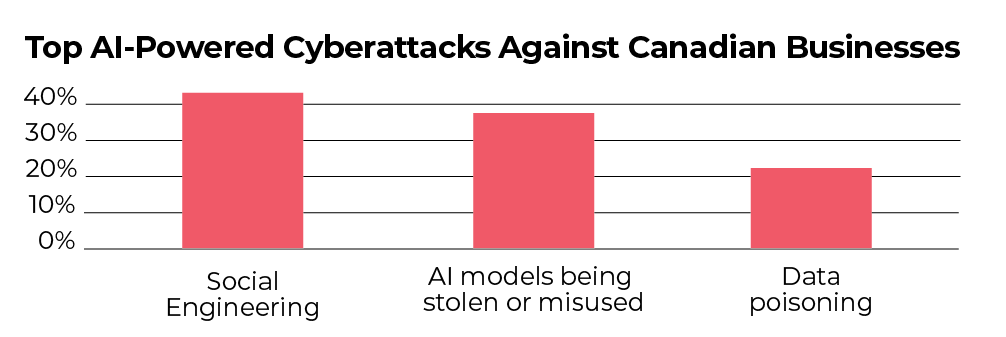

AI is revolutionizing the cybersecurity landscape, and cybercriminals are at the forefront. According to one report, 80% of Canadian organizations experienced an AI-related incident in the past year. Common attacks included using generative AI to create compelling phishing emails and deepfakes; stealing proprietary AI algorithms and datasets; and injecting bad data into organizations’ systems to corrupt AI-decision making.

Regardless of your industry or size, being targeted by a cyberattack is inevitable.

By some estimates, it takes an average of 215 days to recover from a cyber incident, due to the sophistication and incredibly disruptive nature of these attacks.

So, it’s no surprise then that claims analysis from Allianz Commercial found business interruptions account for 50% of insured losses stemming from a cyberattack.

One top of this, other costs associated with technical recovery and incident response following a cyberattack include:

ransomware and data restoration

customer notifications and credit monitoring

brand repair campaigns to rebuild trust

forensic investigations to prevent future attacks

legal ramifications

In today’s digital age, the security and longevity of your business rely on implementing robust cyber defences — including cyber insurance.

“Your cyber response plan has to reflect more than just firewalls and virus protection; it must also include legal, financial and reputational risk mitigations.”

Rob Faiello Client Executive, Commercial Insurance

How to protect your business

Invest in cybersecurity. Work with your Acera Insurance advisor to ensure your coverage matches your specific risk profile, as well as the risk profile for your industry.

Work with a preferred cybersecurity services partner to determine the budget and risk mitigation strategies needed to best protect your business.

Implement AI-powered fraud detection tools.

Conduct regular cyber risk assessments and routinely update your detailed response plan.

Consistently educate your employees on how to identify a cyberattack, especially phishing emails and deepfakes (remember, human error remains the leading cause of cyber incidents against businesses).

Adequate valuations & coverage limits

It is important to ensure your organization’s valuations and coverage limits are keeping pace with rising costs and increasing litigation.

Here are three core areas that require extra scrutiny:

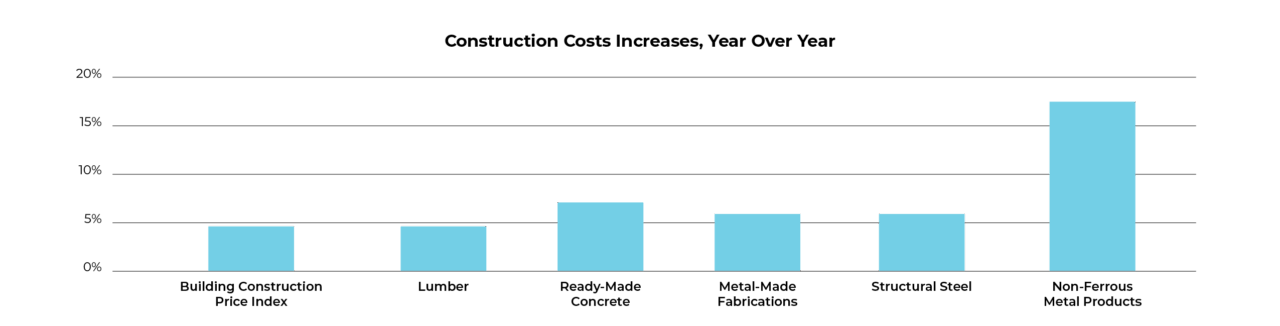

1. Rising replacement costs

Construction and material costs are still on the rise.

What this means for your business

Outdated valuations could leave your property underinsured, potentially leading to claim shortfalls and co-insurance penalties.

How to protect your business

Conduct regular property valuations and update your declared values to reflect current costs.

Evaluate your policy limits to ensure they reflect your company’s growth and inflation.

Use the soft market to your advantage by increasing limits as rates per $100 in value are currently lower.

Business interruption insurance is a lifeline that can help maintain the cash flow needed to keep your business operational when unforeseen events bring things to a halt.

With the escalation of natural catastrophes and severe supply chain disruptions, business interruption has consistently ranked in either the top or second spot of the Allianz Risk Barometer for the past 10 years.

But many Canadian businesses are opting for business interruption insurance limits that are 40% to 60% too low. Flawed worksheet calculations are at least partially to blame for this.

What this means for your business

Selecting an inadequate business interruption limit and indemnity period (the length of time your policy will continue to pay claims) means your business may only receive a fraction of the amount needed to fully recover from a loss.

How to protect your business

Work with an Acera Insurance advisor to leverage professional business interruption reviews. This will ensure you are accurately assessing your business interruption exposures, setting appropriate limits and indemnity periods, and avoiding common pitfalls in worksheet-based calculations.

For complex operations, consider an advisory review for more tailored guidance.

3. Rising employment practices claims

Canada continues to see an increase in the propensity of employees to sue their employers, with claims for wrongful dismissal, workplace harassment, age-related discrimination and constructive dismissal all on the rise.

Civil litigation cases against companies across the country recently increased by more than 10% in a three-year span. Additionally, 48% of surveyed Canadian arbitrators said they’ve experienced an increase in arbitrations in the same period.

What this means for your business

If you have employees, your business can be named in a lawsuit.

Understand and comply with all provincial and federal laws.

Document everything, including employee complaints, performance reviews and disciplinary actions.

Use progressive discipline tactics to address misconduct.

Implement policies that prohibit discrimination.

“Directors and officers insurance for private companies includes very broad employment practices liability coverage, including defence cost coverage at preferential rates.”

Dan Lewis Director, Executive & Specialty Risk

We’re in the business of protecting yours

These key learnings and strategies can help your business prepare for an evolving risk landscape shaped by a soft insurance market, natural disasters, cyber risks and more.

Contact an Acera Insurance advisor to discuss these insights further and to develop a proactive strategy that will help safeguard your business and support your goals in the coming year.

Information and services provided by Acera Insurance, Acera Benefits and any other tradename and/or subsidiary or affiliate of Acera Insurance Services Ltd. (“Acera”), should not be considered legal, tax, or financial advice. While we strive to provide accurate and up-to-date information, we recommend consulting a qualified financial planner, lawyer, accountant, tax advisor or other professional for advice specific to your situation. Tax, employment, pension, disability and investment laws and regulations vary by jurisdiction and are subject to change. Acera is not responsible for any decisions made based on the information provided.

Get a quote.

Simply fill out a few details in our online form and one of our expert advisors will get your quote started.