With roughly two-thirds of adults classified as obese or overweight, Canadians are increasingly expecting their employer health plans to cover weight management drugs. The generic entry of semaglutide in Canada in 2026 may lower the price of the costly specialty drug to finally make this a financially viable option for many employers.

For nearly 30 years, Mike Sanderson has helped Canadian businesses balance employee health and group benefits plan sustainability. Drawing from this tenured experience, Mike explains why generic semaglutide may be the game changing scenario that moves obesity treatment into mainstream chronic disease coverage.

A brief overview of semaglutide and GPL-1 drug coverage

Semaglutide — perhaps better known by the brand name Ozempic — is a GPL-1 prescription medication used to treat Type 2 diabetes.

Yet, the speciality drug made headlines for its notorious off-label use to lose weight due to its appetite suppression affect.

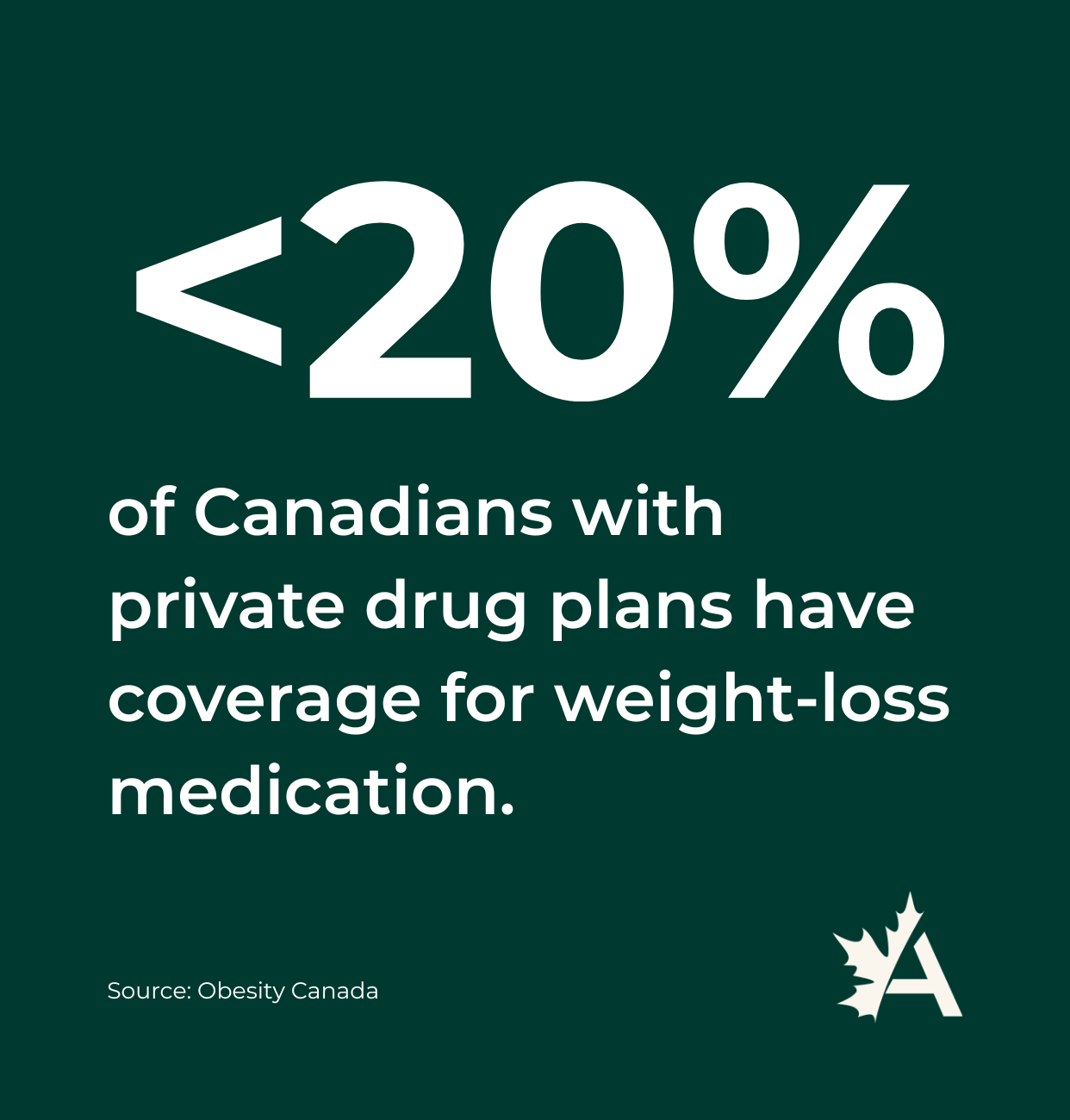

While many group benefits plans provide coverage for semaglutide when used to treat Type 2 diabetes, this is not the case when used for weight management — even after a sister-drug (Wegovy) was developed and exclusively classified as weight loss medication.

This is largely because:

- Employers have historically been hesitant to classify obesity as a disease state.

- The current cost of the specialty drug, which can be upwards of $5,000 a year, presents a significant financial risk for the employer.

Employers are right to carefully approach any high-cost, long-duration therapy — which semaglutide is — especially when the eligible population could be substantial.

But following the recent patent expiration in Canada, the upcoming entry of generic semaglutide is anticipated to drastically cut the drug’s cost. Some estimates are that, once generics are available, the cost will range somewhere between $100 and $150 a month.

Knowing generics are on the horizon, now’s the time for employee group benefits plan sponsors to contemplate an important question: Are we willing to recognize obesity as a disease?

5 reasons group benefits plans should consider obesity as a disease

The most obvious reason is that obesity is a chronic disease.

The stigma surrounding obesity as a lifestyle issue continues to persist. But the World Health Organization, Canadian Medical Association and several provincial medical associations have formally recognize obesity as a chronic disease that deserves medical attention.

Assuming Canadian semaglutide generics significantly minimizes the financial risk for businesses as expected, here are four other cases for covering weight loss treatments in your employee group benefits plan:

Obesity contributes to other chronic diseases affecting employees

Obesity is a risk factor for more than 200 other chronic diseases that require treatments, including:

- Type 2 diabetes

- Osteoarthritis

- Chronic pain

- Sleep apnea

- Depression

- Anxiety

- Dementia

- Cancer

Obesity affects workplace productivity

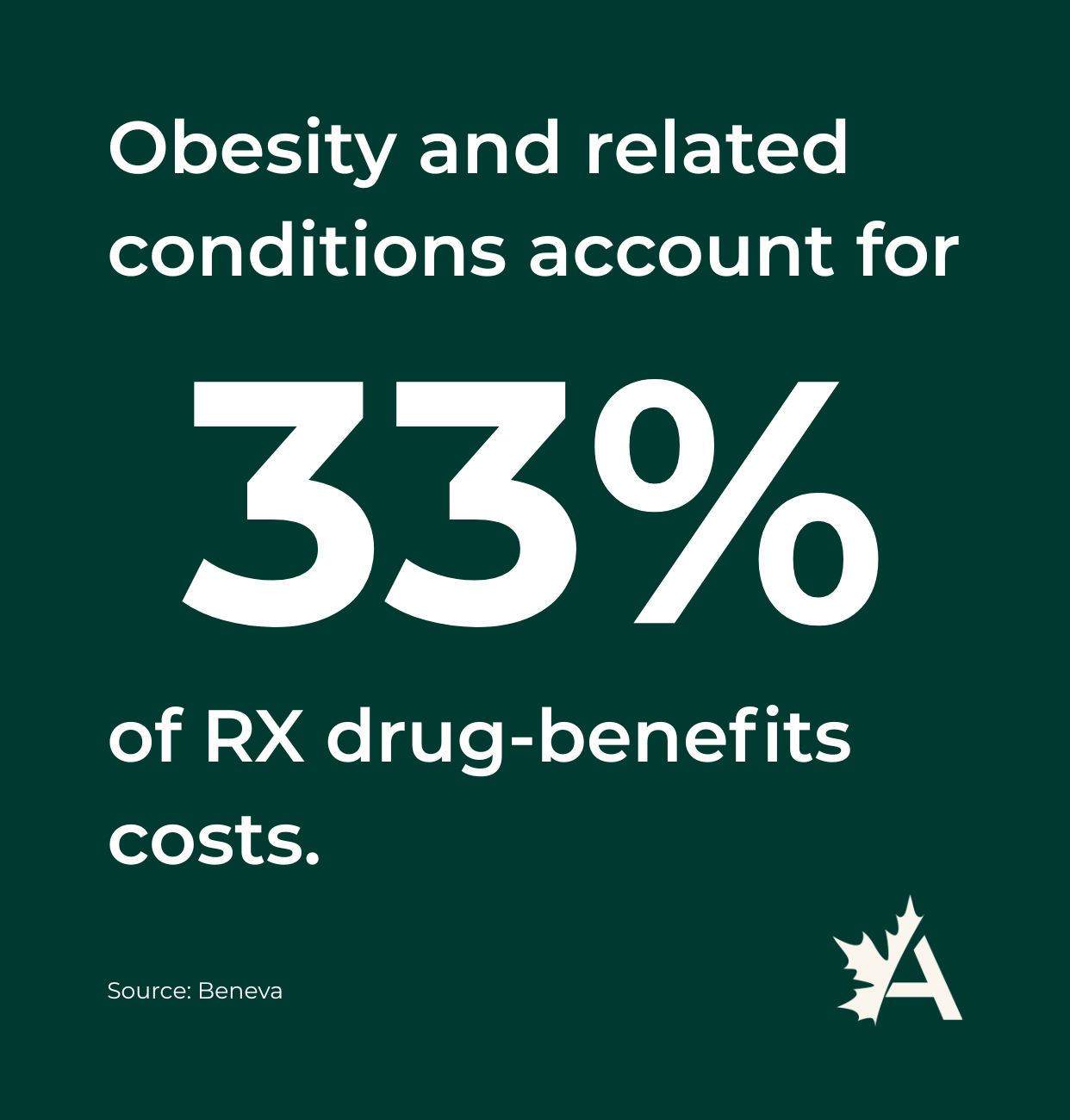

A 2025 study from BMC Public Health calculated the economic impact related to not treating obesity in Canada; among its findings were that indirect costs associated with obesity include:

- $8.2 billion from reduced workforce participation (i.e., people leaving the workforce earlier, reduced ability to work).

- $6.8 billion from presenteeism (reduced energy, focus, mobility, pain, etc. that contributes to lower output).

- $682 million from absenteeism (missed workdays due to health reasons).

Willpower is not an effective obesity treatment

Obesity’s classification as a chronic disease shapes what is considered medically necessary where treatments and benefits insurance are concerned.

Obesity Canada lists three effective interventions for treating obesity:

- Behavioural (i.e., behavioural therapy, nutrition therapy, physical activity)

- Pharmacological (i.e., Health Canada-approved prescription medication, including semaglutide)

- Surgical (i.e., metabolic and bariatric surgery)

Canadians expect their group benefits plan to cover obesity treatments

Benefits Canada’s Healthcare Survey 2025 report found:

- 65% of plan members agree that weight loss medications are an important obesity treatment.

- 51% of plan members who feel they need to or have been told to lose weight are interested in taking weight loss medications.

- Of those plan members interested in taking medication to lose weight, 66% believe their group benefits plan should cover “most or all of the cost.”

To summarize: Your organization is likely already absorbing obesity-related expenses through lost productivity and indirect costs associated with treating other chronic conditions. Covering treatments specifically for weight loss could reduce downstream claims and disability risk over time.

Canadian semaglutide generics may make obesity treatment coverage common in employer health plans

We may be approaching a blockbuster moment for GLP-1s, where affordability forces clarity on obesity coverage in group benefits plans.

Covering semaglutide for weight loss in employee group benefits plans has understandably been treated with caution up to this point, speaking solely from a financial risk management perspective.

This is because the current high cost of semaglutide (a drug that needs to be taken continuously for a long period) and likely high utilization (based on obesity rates in Canada) could put plans at risk of rapid cost escalation.

But if current estimates prove true, and generic semaglutide drives the drug cost down by 50% to 70%, the question for plan sponsors becomes: Can you afford not to cover obesity directly?

FAQs: Canadian semaglutide generic and employer health plans

No, generic entry does not automatically change coverage. But the high interest for weight loss drugs may expediate things. Any expansion will ultimately depend on insurer strategy, provincial formulary decisions and employer choice.

Whether to recognize obesity as a disease state is a foundational decision for employers because it determines whether covering GLP‑1 drugs can be justified as a legitimate medical expense rather than a discretionary or lifestyle benefit. Plan sponsors have to consider the financial risk management against better health outcomes for their employees.

Because employees are demanding it.

Many plan sponsors are receiving frequent questions from employees asking why weight-loss drugs like semaglutide (Wegovy) are not covered under their benefits plan despite being widely perceived as an effective treatment.

While generic drugs lower costs, cost control remains an important strategy for plan sponsors. That said, we’re waiting to see how provincial plans will include generic semaglutide in their formularies, which usually dictates how private healthcare plans add the drug as part of their formulary management. We’re also waiting to see what cost-containment strategies insurance carriers outline, such as step therapy, prior authorization and specialty dispensing. Once these details are public, the best approach is to speak with your Acera Benefits consultant to determine next steps.

Share this article:

As a group benefits, savings and wellness advisor, Mike Sanderson helps businesses create effective and measurable programs that align with their organization values, goals and budgets. With a passion for development of unique employee rewards plans, Mike is an expert in plan architecture. Mike began his career in 1997 and has held various roles in the employee benefits space, including product development for a number of large Canadian insurers. As part of the Acera Benefits division, Mike is dedicated to delivering an exceptional client experience, a transparent process for measuring ROI, cost efficiencies and best practices for employee onboarding and ongoing employee engagement.

You can reach Mike at 250.869.3921 or mike.sanderson@acera.ca.

Related reading:

- 2026 group benefits outlook

- 5 ways employers can improve their employee wellness programs

- The millennial-led transformation of employee benefits plans

Information and services provided by Acera Insurance, Acera Benefits and any other tradename and/or subsidiary or affiliate of Acera Insurance Services Ltd. (“Acera”), should not be considered legal, tax, or financial advice. While we strive to provide accurate and up-to-date information, we recommend consulting a qualified financial planner, lawyer, accountant, tax advisor or other professional for advice specific to your situation. Tax, employment, pension, disability and investment laws and regulations vary by jurisdiction and are subject to change. Acera is not responsible for any decisions made based on the information provided.

Get a quote.

Simply fill out a few details in our online form and one of our expert advisors will get your quote started.